Grains finally catch a bullish bid into Labor Day weekend

Happy Labor Day weekend market watchers!

Out goes August, in comes September and all the while with October weather! We’ll take every bit of it! The abundant rain, in most areas, and cooler temperatures to close out what is typically the hottest month of the year is well outside of any semblance of normalcy.

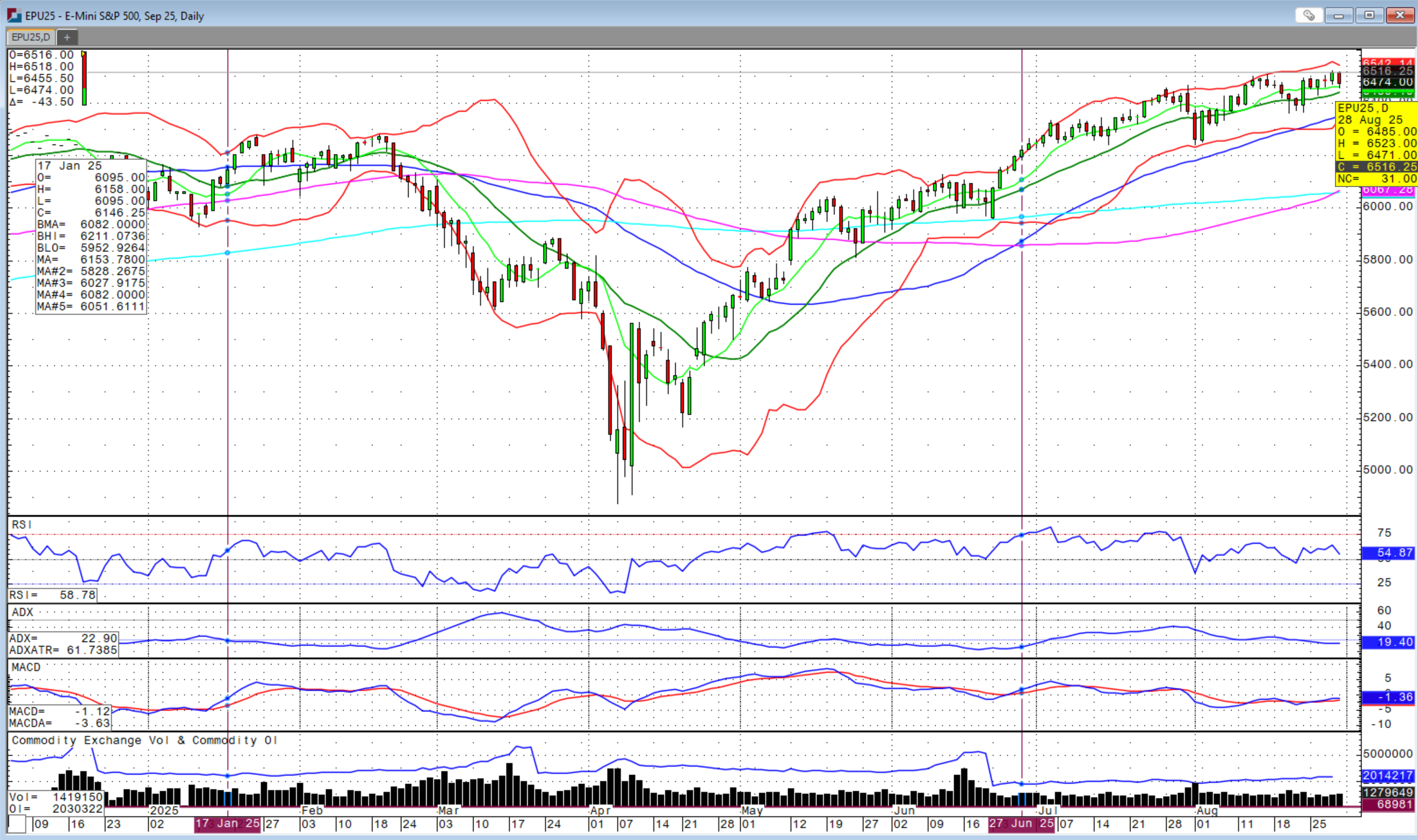

Equity markets chopped sideways this week while the S&P 500 managed to eek out a new, all-time high on Thursday. While there is much optimism for a September interest rate cut by the FOMC amid much controversy stirred up by President Trump over the past several months, the Fed’s preferred inflationary gauge, the core Personal Consumption Expenditures (PCE) index excluding food and energy for July came in at 2.9 percent annually, in line with expectations, but the highest since February.

Consumers all around are in tight positions and many are struggling, but the data keeps pointing to strength, making the case against interest rate cuts. When will these two stories converge and which side is closer to the true situation? It seems that some post-Labor Day weekend squeeze could emerge as the officially unofficial end to summer is here. The holidays are approaching and that will be the real test of consumer strength. The tariffs have created conundrums for retailers and added cost. Will consumers see higher costs during the holidays, and will they be able to afford it? Watch the jobs data these next couple months as that is beginning to show signs of softness that could be the real catalyst to stall this consumer. However, until then, the cattle markets continue to run wild, literally.

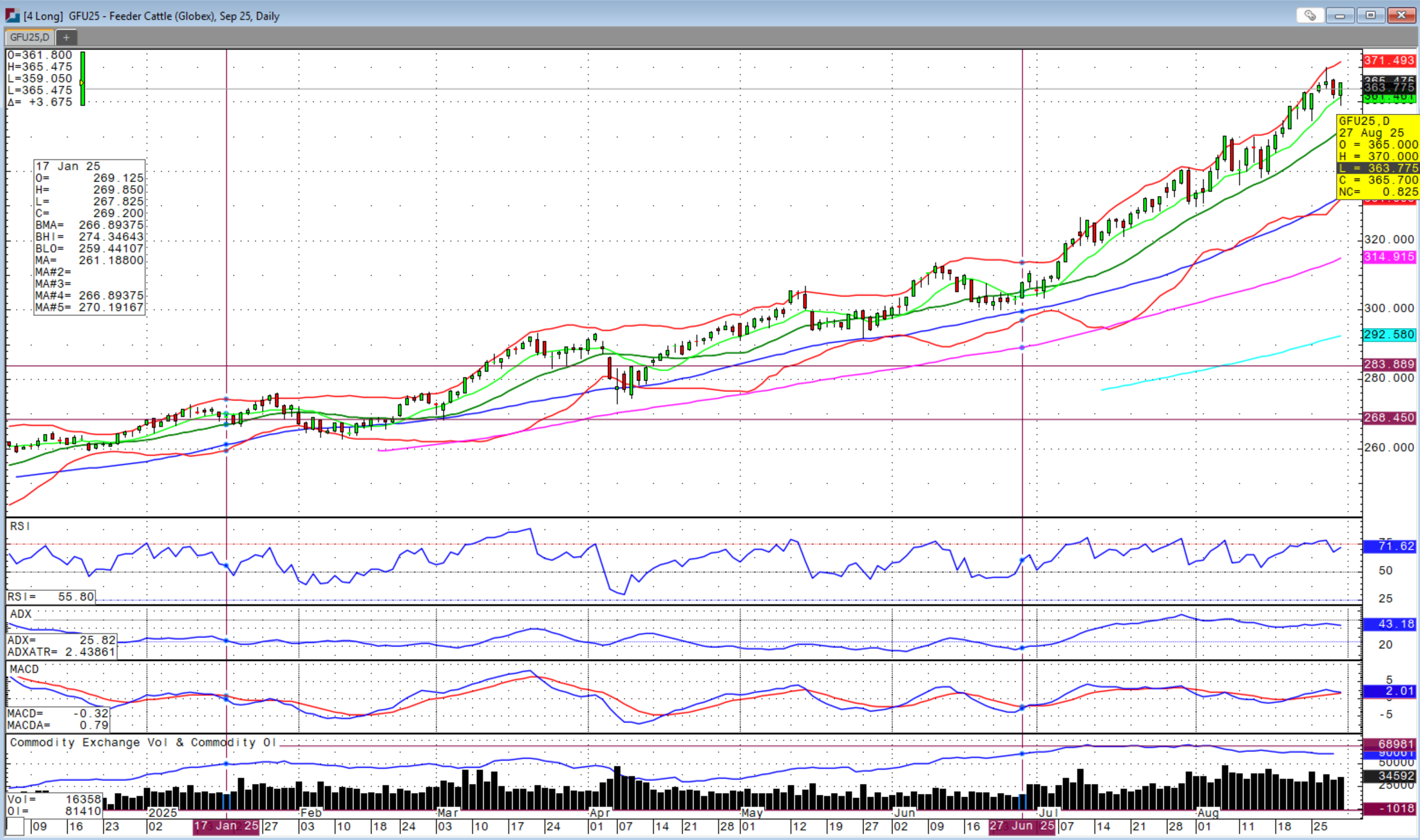

The mid-week peak that saw September feeder contracts spike to exactly $370.000, seemed unable to stop. August feeders expired Thursday at noon at $366.000, while other contracts weakened to the 9-day moving average, a level well supported since late June. The Friday session started off on a weaker tone with many expecting we could see a material selloff given the end of the month leading into a long weekend, but it turned out to be anything but. After some two-sided trade, contracts actually began to surge into the close and closing at the high. The remaining 2025 feeder contracts did not make a high above Thursday’s high, but the 2026 contracts did. Together with a low below Thursday’s low, that has the 2026 feeder contracts putting in an outside reversal higher day. We will have to wait to see how strong the momentum trade is on Tuesday once the markets reopen at 8:30 AM.

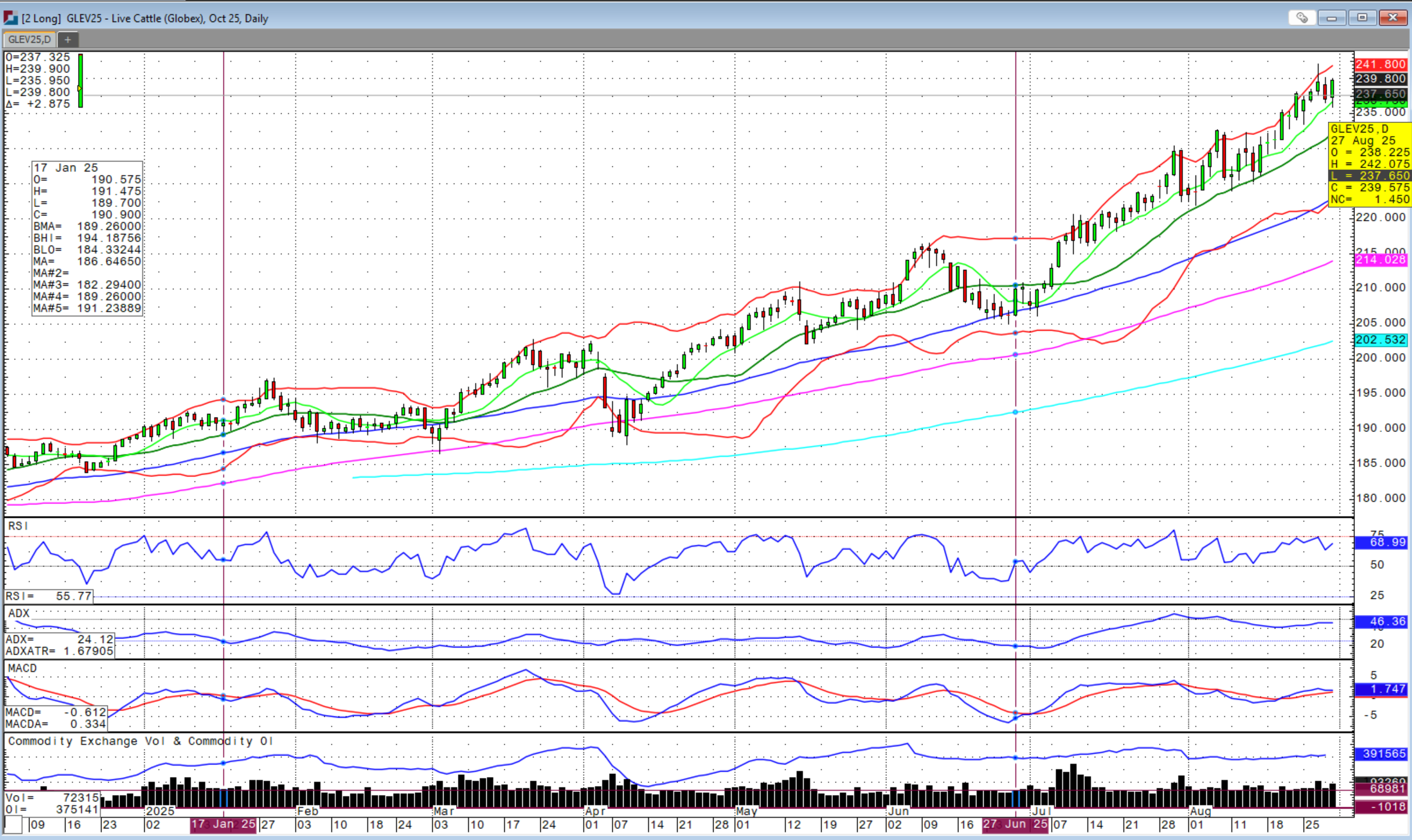

Cash fed cattle were the highlight to close the week with a new record $242 traded in Texas and $245 traded again in Nebraska. The spread between southern and northern bids has drastically narrowed and could indicate some topping action in the willingness of packers to pay more. But do they have a choice? That’s what the feedlots deny as they continue to be in the driver’s seat. Know that plenty of games are being played among the packers to try and outlast the weaker packers in this environment of negative margins. The cattle market has been crazy, but as they say, markets can be irrational longer than ‘you’ can stay liquid. If you’re staying short, risk manage with call options as I don’t think we’re done yet based on Friday’s move. However, absolutely anything can happen in this market environment without forewarning.

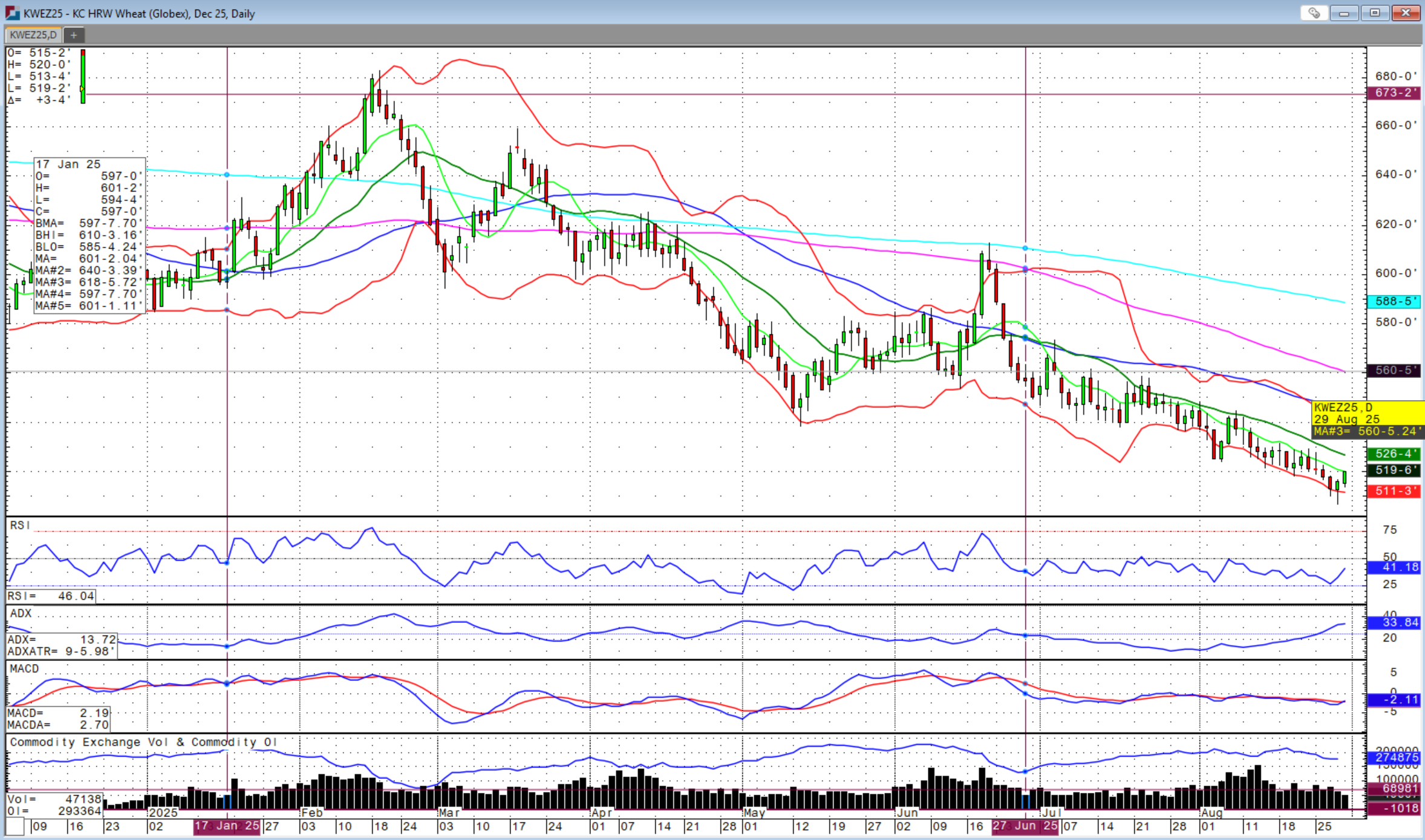

The grain markets are finally showing signs of life worth talking about. Thursday’s outside reversal higher day followed by Friday’s breakout higher above the 50-day moving average showed some encouraging signs. The above chart gap from July 3rd is at $4.32 ¾, just above the 100-day moving average. While more talk of disease issues and flash droughts are emerging in parts of the corn belt, expect there to be a lot of farmer selling on any significant rallies especially with weak basis levels.

The other factor playing into this is the falling basis in soybean cash bids given the lack of China business. This may lead to farmers needing to store soybeans versus corn and therefore selling more cash corn now through harvest in addition to the large crop in the field. US corn conditions held steady at 71 percent Good-to-Excellent (G/E), one percent ahead of expectations, and remains the best in 9 years. US soybean conditions improved one percent from last week, but two percent above expectations, now also the best in 9 years for late August.

We are beginning to see cross border diplomatic activity and headlines between the US and China regarding negotiations, creating expectations for dialogue and deals. This could be bullish for soybeans as everyone knows by now that China’s lack of any US soybean purchases is being kept as a card to play in negotiations. In fact, China announced buying soybeans from uncommon origins this week to further display its options. A deal and dialogue would be bullish for soybeans, but the lack thereof could be bearish. Much will also depend on the potency of US biofuel policy.

The US dollar weakness is supportive for the commodity complex, but it still requires global demand. The metals market saw plenty of that with new highs in silver and a spike in gold contracts. Could this also be a move to safe haven assets for volatility to come? Something is up that we will have to monitor in this next shortened week of trading with US equity and ag markets closed Monday for Labor Day weekend in the US. The wheat market benefited from the rally in corn and the weaker US dollar.

Seasonally, we typically find some strength this time of year after a post-harvest selloff. This week last year was the bottom followed by a near $1.00 rally into the end of September. Let’s hope there is some continued strength ahead in the grain markets after the recent weakness well below breakeven levels for producers. If you need to sell grain at these levels, take a small portion of the cash grain check and re-own those bushels on the Board. Option volatility is low as are prices and so call options are very reasonable as is the time value to go out to March contracts.

If you need to sell to pay bills, that doesn’t mean you have to be out of the market and watch it rally. You can stay in the game without owning the physical bushels and having to pay storage. Just buy the call option for a fraction of what it cost to own the physical bushels and stay in the game. Yes, there is terminology involved, but that’s why Sidwell Strategies is here. Just give us a call and we will advise and execute on how to achieve your cash flow needs and profit margin goals. Reach out and use the tools that are there for you instead of blindly holding grain and paying elevator storage until you absolutely have to sell it. Once you see the numbers and ability to do more with less, you will not be able to unsee it. US spring wheat conditions declined this week in the final condition rating of the year and could add some underlying support to this market. Ultimately, we need the managed funds to cover shorts and be buyers in the grain complex, which I believe is about to take place at least to some degree.

Sidwell Strategies is the one-stop shop to protect cattle with futures, puts, LRP or a combination of all, which is probably the best strategy overall. If you’re ready to trade commodity markets, give me a call at (580) 232-2272 or stop by my office to get your account set up and discuss risk management and marketing solutions to pursue your objectives. Self-trading accounts are also available. It is never too late to start and there is no operation too small to get a risk management and marketing plan in place.

Wishing everyone a successful trading week! Let us know if you'd like to join our daily market price and commentary text messages to stay informed!

Brady Sidwell is a Series 3 Licensed Commodity Futures Broker and Principal of Sidwell Strategies. He can be reached at (580) 232-2272 or at brady@sidwellstrategies.com. Futures and Options trading involves the risk of loss and may not be suitable for all investors. Review full disclaimer at https://www.sidwellstrategies.com/fccp-disclaimer-21951.